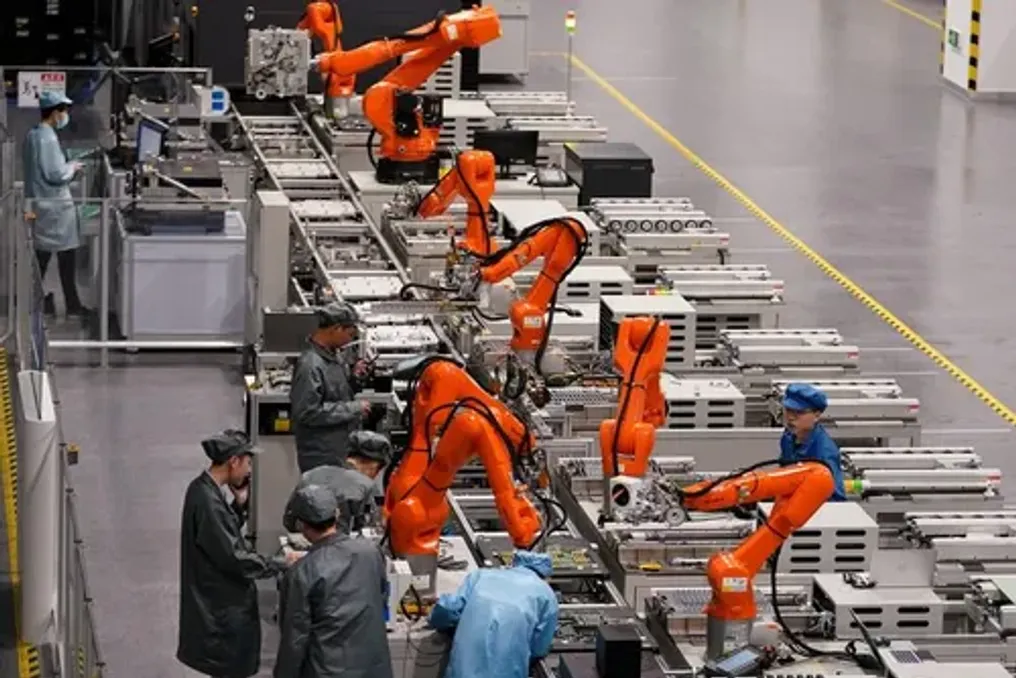

Manufacturing companies are actively implementing artificial intelligence, but industry specialists emphasize that existing financing models must transform to support digital modernization and enhance the competitiveness of enterprises.

Challenges for South Africa's Manufacturing Sector

Small and medium manufacturing enterprises in South Africa are encouraged to adopt smart manufacturing and artificial intelligence technologies at a pace appropriate to their business processes. However, access to suitable financing is a critical factor in the speed of this transition. This call came amid growing pressure on manufacturers who are forced to modernize production while simultaneously managing declining output volumes, increased costs, and heightened customer demands for digital traceability and compliance.

The South African manufacturing sector contributes nearly 11% to the country's gross domestic product and was one of the three sectors that created jobs in the first quarter of 2026. Nevertheless, the sector has recorded two consecutive quarters of production decline, which underscores the necessity of improving business efficiency and competitiveness.

Financing Challenges for Digital Transformation

During a panel discussion on Industry 4.0, focusing on artificial intelligence, digitalization, automation, and smart manufacturing at the Manufacturing Indaba 2026 event, Product Manager Lula Koreshini Pillay noted that many manufacturers initially focus on the technology itself, neglecting the necessary financing for digital transformation. According to her, SMEs begin discussions about smart manufacturing by concentrating on technologies. Yet, every system upgrade, sensor, or traceability platform requires upfront costs whose return only materializes months later.

Pillay added that finding financing that accounts for the specific cash flow characteristics of manufacturing, rather than traditional lending methods, is a more complex task. She pointed out that the market needs to answer the question of modernization costs and who will finance this transition. Although manufacturers are advised to approach IDC for expansion or SEFA for guarantees, neither option solves the problem. Material and technology costs arise now, while the revenue they generate arrives only after several months. Creditworthiness verification must be based on real-time transaction data and SME inflow patterns so that working capital can be structured according to the realities of the factory floor.

Current State of AI Adoption

Research also indicates that the adoption of AI among South African companies is already well underway. According to the News24 x Lula small business survey, based on responses from 1088 SME owners in January of this year, over two-thirds of South African enterprises either use AI daily or are actively experimenting with the technology. Manufacturers are increasingly using AI to optimize production lines, reduce waste, and improve operational efficiency, thereby meeting growing customer demands for digital traceability and regulatory compliance.

However, timeliness remains a major obstacle. Typically, manufacturers begin inventory preparation in the second half of the year to meet peak demand in retail, wholesale, and logistics in September, October, and November. This means companies have to invest in equipment, software, cybersecurity systems, machine upgrades, and staff training long before receiving income.

In Pillay's view, delays in securing funding can ultimately affect a manufacturer's ability to secure future contracts and remain competitive. She noted that there are numerous expense categories in this modernization gap: sensors, monitoring systems, software licenses, equipment upgrades, cybersecurity, traceability platforms, and skills development—all competing for limited capital.

Mismatch with Traditional Banking Models

Garth Rossiter, Director of Credit and Capital at Lula, stated that traditional credit models often fail to recognize the unique cash flow cycle of manufacturing enterprises. He emphasized that traditional banks tend to analyze reports and historical financial information from the previous year, but this does not reflect the actual functioning of a factory.

Rossiter explained that if a business owner spends money on raw materials in July but won't see revenue until November, they require financing that understands this interim period. Operational modernization is no longer an optional measure—it is a matter of survival. The winners are those manufacturers who find financial partners that align with the real rhythm of their trade. He added that financing products built around projected cash flow could help manufacturers invest in technology without placing excessive strain on working capital.

Lula reported having provided over 3,300 manufacturing enterprises with more than 3 billion early payments to date. The average advance received by manufacturers is 203,000 rand, making this sector the second largest for the company in terms of financed volume. Rossiter concluded that quick access to finance can determine whether manufacturers can successfully modernize or lose opportunities to competitors. He stressed that the ability to obtain funding precisely when an opportunity arises allows plans not to be postponed, but to actually be realized, which is the key difference between a growth plan on paper and real scaling.

Industry stakeholders believe that financial solutions adapted to manufacturing cycles can play a vital role in supporting SMEs in adopting AI, increasing productivity, and strengthening South Africa's industrial competitiveness.